Review Umbrella Support

Understanding Insurance: Protecting Your Future and Financial Assets

Knowing about insurance is vital for everyone who wants to secure their financial stability. It provides a safety net that shield against sudden occurrences potentially causing substantial damage. A wide range of coverage options exists, each designed for different needs. However, many individuals struggle figuring out the necessary extent of coverage or understanding the fine print of the agreement. The complexities of insurance can create uncertainty, necessitating a better grasp of the most effective way to secure assets. What should one consider before making a decision?

Insurance 101: Essential Information

Insurance serves as a financial safety net, guarding individuals and enterprises from unforeseen risks. Insurance is primarily a covenant connecting the policyholder and the provider, where the customer pays a regular charge in exchange for financial coverage covering defined damages or setbacks. The essence of insurance lies in risk management, allowing individuals to transfer the burden of potential financial loss to an insurer.

The policies specify the requirements and provisions, specifying the scope of protection, what is excluded, along with the process for submitting claims. The concept of pooling resources is central to insurance; many pay into the system, which enables the payment of benefits to those who incur damages. Understanding the basic terminology and principles is crucial for choosing wisely. Ultimately, insurance intends to give reassurance, ensuring that, in times of crisis, individuals and businesses can recover and continue to thrive.

Insurance Categories: A Comprehensive Overview

Numerous forms of coverage are available to cater to the diverse needs of individuals and businesses. The most popular types include health coverage, designed to handle doctor bills; auto insurance, protecting against vehicle-related damages; as well as property coverage, securing assets from perils such as theft and fire. Life coverage provides monetary protection for dependents if insightful guide the insured passes away, whereas income protection offers salary substitution if one becomes unable to work.

For companies, professional indemnity shields from accusations of wrongdoing, while commercial property coverage protects tangible goods. Professional liability coverage, or simply E&O insurance, protects professionals from demands arising from negligence in their duties. Additionally, travel insurance provides coverage for unforeseen incidents during travel. All insurance policies plays an essential role in managing risks, ensuring individuals and businesses can mitigate potential financial losses and ensure stability during unpredictable times.

Evaluating Your Coverage Requirements: What Level of Protection is Sufficient?

Determining the appropriate level of necessary protection demands a detailed review of property value and possible dangers. One should review their financial situation and the possessions they aim to cover to arrive at an adequate coverage amount. Sound risk evaluation methods are fundamental to guaranteeing that one is not insufficiently covered nor paying extra for needless protection.

Appraising Your Possessions

Assessing the worth of assets is an essential step in knowing the required level of protection to achieve adequate insurance coverage. This process involves establishing the price of private possessions, real estate, and monetary holdings. Property owners must evaluate elements like the present economic climate, reconstruction expenses, and depreciation when appraising their property. Furthermore, one must appraise private possessions, vehicles, and potential liability exposures linked to their possessions. By completing a detailed inventory and assessment, they can identify areas where coverage is missing. Also, this appraisal allows individuals customize their insurance plans to address particular needs, guaranteeing sufficient coverage from unanticipated incidents. Finally, accurately evaluating asset value lays the foundation for smart coverage choices and economic safety.

Methods for Evaluating Risk

Establishing a thorough understanding of asset value naturally leads to the next phase: determining necessary insurance. Risk evaluation techniques entail identifying potential risks and figuring out the right degree of insurance required to mitigate those risks. This process begins with a detailed inventory of assets, such as real estate, vehicles, and private possessions, alongside an analysis of potential liabilities. The individual must consider elements like location, lifestyle, and industry-specific risks that could influence their insurance needs. Additionally, checking existing coverage and identifying gaps in coverage is vital. By measuring potential risks and aligning them with the value of assets, you can make educated choices about the amount and type of insurance necessary to secure their future reliably.

Interpreting Coverage Jargon: Key Concepts Explained

Knowing the policy provisions is crucial for traversing the complexities of insurance. Core ideas like coverage categories, insurance costs, out-of-pocket limits, policy limits, and limitations play significant roles in judging how well a policy works. A firm knowledge of these terms helps individuals make informed decisions when picking insurance choices.

Types of Coverage Defined

Coverage options offer a selection of different coverages, each designed to address specific risks and needs. Standard coverages are coverage for liability, which shields from legal action; property coverage, securing tangible property; and coverage for personal injury, which addresses injuries sustained by others on the policyholder's premises. Moreover, comprehensive coverage gives defense against a variety of threats, including theft and natural disasters. Niche protections, such as professional liability for businesses and medical coverage for people, further tailor protection. Understanding these types helps policyholders choose the right coverage based on their unique circumstances, providing proper defense against future fiscal setbacks. Every coverage category is vital in a comprehensive coverage plan, finally resulting in monetary safety and serenity.

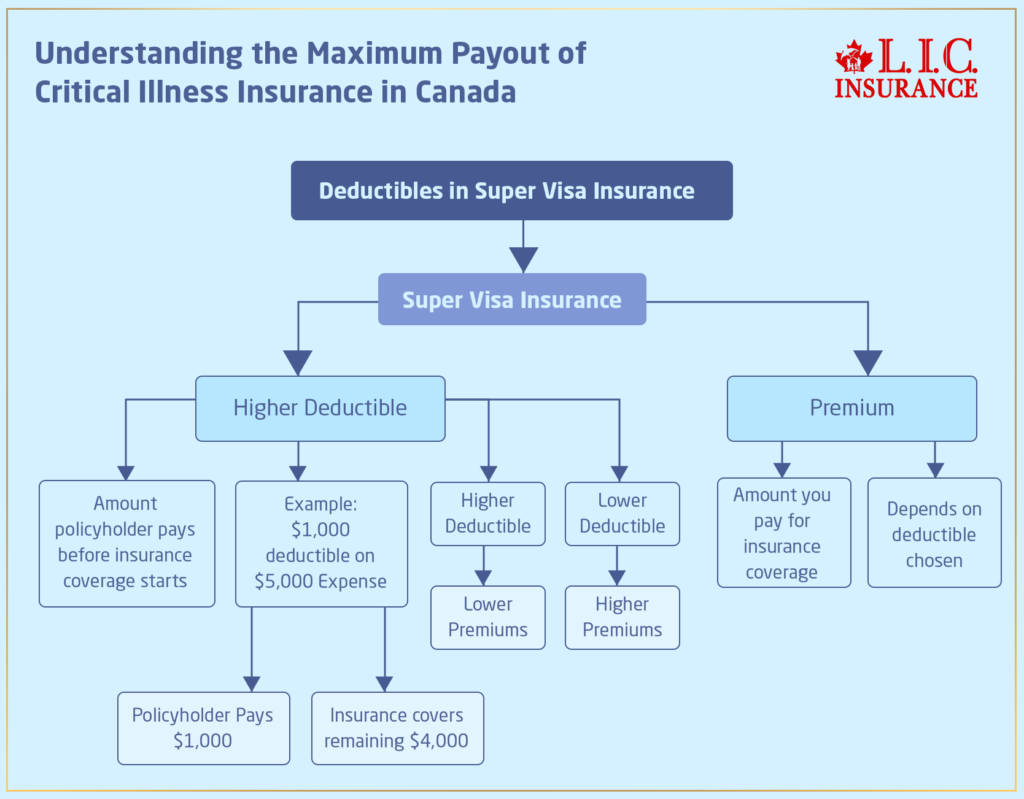

Premiums and Deductibles

Selecting the right coverage types is just one aspect of the insurance puzzle; the monetary elements of deductibles and premiums also greatly influence policy decisions. Premiums represent the cost of maintaining an insurance policy, usually remitted yearly or every month. A larger premium usually corresponds to broader protection or lower deductibles. In contrast, deductibles are the amounts policyholders must pay out-of-pocket before their insurance coverage kicks in. Choosing a higher deductible can lower premium costs, but it could result in more fiscal liability during claims. Understanding the balance between these two elements is vital for those aiming to protect their assets while handling their finances efficiently. Fundamentally, the interplay of the costs and payouts defines the overall value of an insurance policy.

Limitations and Exclusions

What elements that can hinder the efficacy of an insurance policy? Policy limitations within a policy specify the conditions under which coverage is unavailable. Typical exclusions include pre-existing conditions, acts of war, and some forms of natural calamity. Caveats might also be relevant to maximum payout figures, making it essential for policyholders to recognize these restrictions in detail. These elements can considerably affect claims, as they determine what financial setbacks will not be compensated. Policyholders must read their insurance contracts carefully to find these restrictions, so they are well aware about the extent of their coverage. A clear grasp of these terms is essential for protecting one's wealth and long-term financial stability.

Filing a Claim: What to Expect When Filing

Making a claim can often feel overwhelming, especially for those unfamiliar with the process. The initial step typically requires informing the insurance company of the incident. This can usually be done through a telephone call or web interface. When the claim is submitted, an adjuster may be appointed to evaluate the situation. This adjuster will examine the specifics, collect required paperwork, and may even inspect the location of the event.

Once the review is complete, the insurer will determine the validity of the claim and the payout amount, based on the terms of the policy. Claimants should expect to provide supporting evidence, such as receipts or photos, to help the review process. Communication is essential throughout this process; you may have to contact with the insurer for updates. Ultimately, understanding the claims process allows policyholders to manage their rights and responsibilities, to guarantee they obtain the funds they deserve in a timely manner.

Guidelines for Finding the Right Insurance Provider

How do you go about finding the most suitable insurance provider for their circumstances? To begin, they need to determine their unique necessities, considering factors such as coverage types and spending restrictions. It is crucial to perform comprehensive research; web-based feedback, evaluations, and client feedback can provide information about customer satisfaction and service quality. In addition, getting estimates from several insurers allows one to compare premiums and the fine print.

One should also assess the financial stability and standing of potential insurers, as this can impact their ability to settle claims. Engaging in conversations with agents can clarify policy terms and conditions, providing clarity. In addition, seeing if any price reductions apply or combined offerings can increase the worth of the policy. Lastly, seeking recommendations from trusted friends or family may help uncover dependable choices. By following these steps, people are able to choose wisely that are consistent with their insurance needs and budgetary aims.

Staying Informed: Ensuring Your Policy Stays Relevant

After selecting the right insurance provider, individuals must remain proactive about their coverage to make certain it addresses their changing requirements. Periodically examining the coverage details is necessary, as shifts in circumstances—such as tying the knot, buying a house, or career shifts—can affect what coverage is needed. Policyholders must plan annual reviews with their insurance agents to review possible modifications based on these personal milestones.

In addition, keeping current on industry trends and shifts in policy rules can give helpful perspectives. This information might uncover new insurance possibilities or discounts that could enhance their policies.

Monitoring the market for competitive rates may also lead to more cost-effective solutions without reducing coverage.

Frequently Asked Questions

How Do Insurance Premiums Vary With Age and Location?

Insurance premiums generally go up based on age due to increased risks associated with senior policyholders. Additionally, location impacts rates, as cities usually have steeper rates due to a greater likelihood of accidents and crime compared to non-urban locations.

Am I allowed to alter My Insurance Provider Mid-Policy?

Yes, individuals can change their insurance provider mid-policy, but it is necessary to check the conditions of their present plan and guarantee they have new coverage in place so they don't have lapses in coverage or associated charges.

What Happens if I Miss a Premium Payment?

Should a person fail to make a premium payment, their insurance coverage may lapse, which can cause a gap in security. The coverage might be reinstated, but it might demand retroactive payments and might incur fees or more expensive coverage.

Will existing health problems be covered in medical policies?

Pre-existing conditions may be covered in health plans, but the extent of protection differs per policy. Numerous providers enforce a waiting time or specific exclusions, while others may provide immediate coverage, stressing that policy details must be examined completely.

What is the impact of deductibles on My Insurance Costs?

Deductibles affect the price of insurance by setting the sum a holder of the policy is required to spend before the plan begins paying. If deductibles are higher, monthly premiums are usually lower, and a smaller deductible causes higher payments and possibly fewer personal costs.